08/04/2014

In November last, we started writing an in-depth plan as guidance for the UK in leaving the EU, the basis of which has been published

here, where you will also find the references to the issues discussed here.

At the time the submission was so

arbitrarily rejected, however, I observed that my single, most important contribution was the observation that "Brexit" should not be regarded as a single event, but a process â rather like the process of European integration, with its progression of treaties.

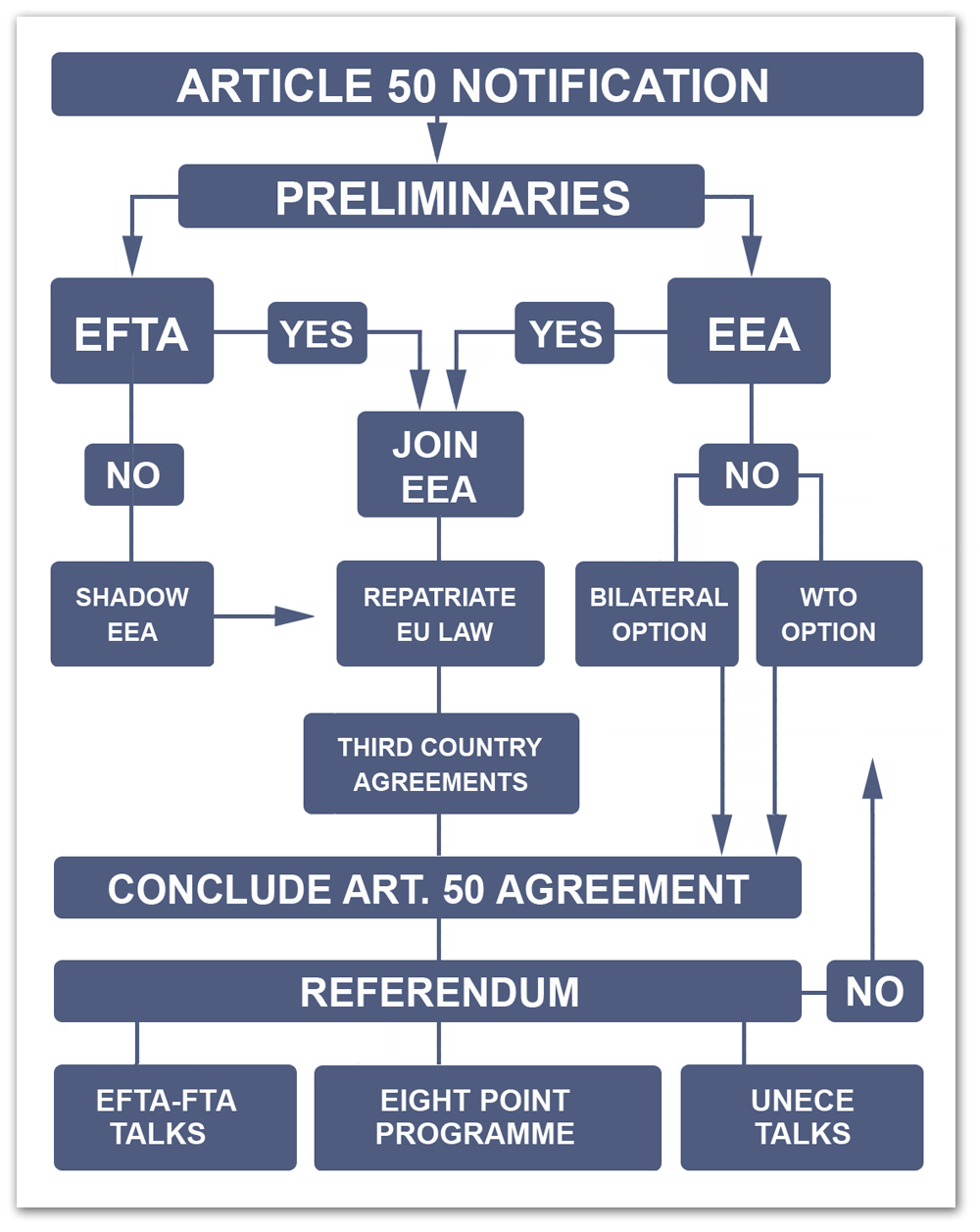

Thus, I advanced that we should not be looking for a single product, a finished "plan" which we could park in the showroom and polish, for all to admire. Rather, we should be setting out a series of ongoing strategies, an exit to which would be added FLexible response and Continuous development. Thus, in our submission, "Brexit" became "FLexCit" â with a flow chart illustrated above.

As to the agreement arising from the Article 50 negotiations, this became not an end point, but simply one step in a long-drawn-out process that involves nothing more than a series of interim solutions. Thus, we argue that Britain should rejoin EFTA and, through that, the EEA.

This would involve adopting the entire Single Market

acquis, essentially the "Norway option", allowing us to continue trading with our EU neighbours without interruption. But we would also repatriate the rest of the

acquis and, with very few exceptions, re-adopt them into UK law (alongside repealing the ECA). Then, we would need a provision by which we would adopt the EU's bilateral treaties, to maintain the status of the third country agreement, once we have left the EU.

This three-point plan offers stability and continuity. In effect, the day after we leave the EU will be little different, in practical terms, from the day before we leave. There will be no Armageddon â no end of the world scenario. The Europhile FUD will simply not materialise.

However, that means that, in terms of tangible dividends, there will be very little to see. Much has been made of the reduced burden of regulation that might be expected but our analyses suggest that expectations might be unrealised in the short-term.

Much of the existing legislation will have to be maintained, either because of EEA membership, domestic regulatory requirements or international obligations. The dividend, we believe, will not come from "big bang" deregulation, but from continuous development, majoring on the issues we have raised.

What you will see from the flow chart though, right at the bottom, are three blocks. One is headed "EFTA/EEA talks", the other the "eight-point programme" and the third "UNECE talks".

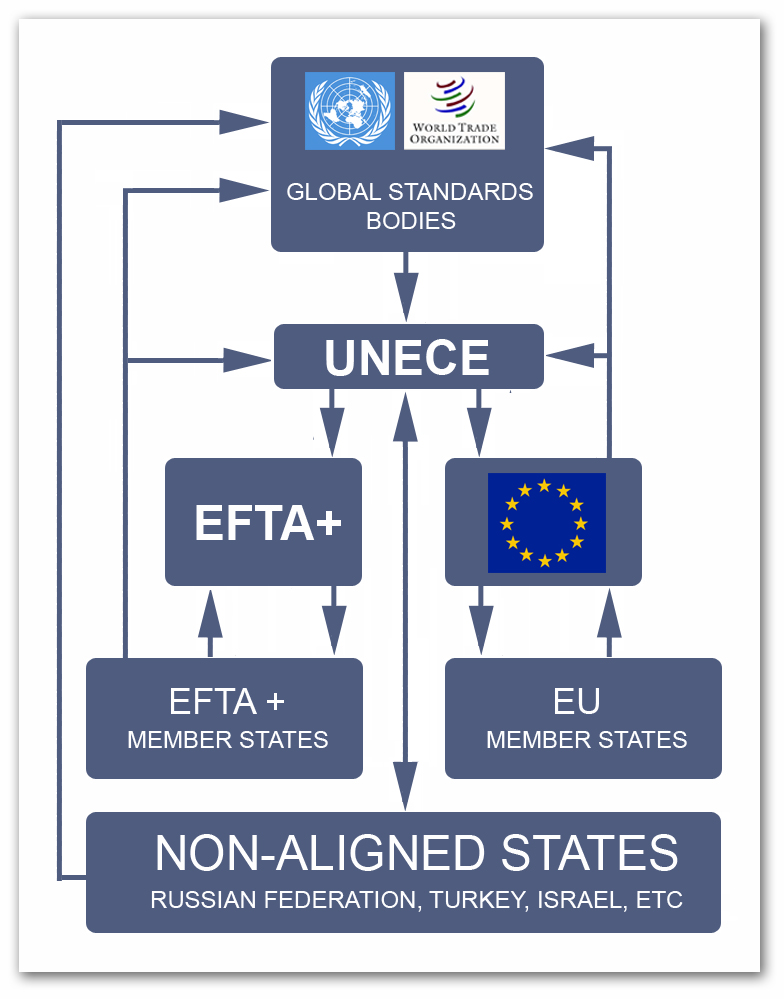

The first and the third of the blocks are linked, and I will deal with these in more detail in a separate post. In essence, though, I propose that the EEA is eventually abandoned, and that EFTA becomes a much more powerful and wide-ranging free trade area, perhaps taking on more countries, and even other former EU countries, becoming what I call EFTA+.

I then suggest that the EU ceases to be the custodian of the Single Market

acquis, and is replaced by UNECE, to become a genuine European single market, covering the whole of Continental Europe, built around the WTO TBT Agreement and, in particular, Article 2.4. Thus we have a completely different structure for the Single Market, as illustrated immediately above, removing political integration from the mix.

This then leaves the "eight-point plan", the elements of which are set out on the chart below. Firstly, we have posited that withdrawal from agriculture, fishing, regional and other policy areas will eventually allow for the repeal of some measures and their replacement with more efficient policies.

Secondly, we argue that better regulation, with risk-related measures, could yield significant economies, especially when combined with better, more timely intelligence.

Third, we aver that greater attention must be given to system vulnerabilities and to improved enforcement if growth in transnational organised crime is to be contained. This is a very significant check on the growth of free trade, as organised crime moves in to take advantage of the systems in place.

The proliferation of free trade zones, for instance, facilitates crime and tax avoidance. FTAs are also responsible for increased cross-border crime. Yet relatively little attention is being given to the problems.

Here, there is an interesting contrast between TTIP, which aims to "boost" the global economy by around â¬310bn, and TOC income estimated at more than $3trn a year. International trade in counterfeited goods and piracy alone is estimated to grow from $360bn (based on 2008 data) to as much as $960bn by 2015.

As to the fourth element, we need to be seeking regulatory convergence, leading to global regulatory harmonisation and the elimination of duplication. This could have a very substantial effect in reducing costs, provided it is done sensibly.

On the other hand, between markedly different regulatory environments, hysteresis can negate any beneficial effects of convergence. In fact, the hysteresis effect would rule out free trade areas based on the Commonwealth, and/or mixes of other countries where there are major differences between social development.

Fifth, we need better dispute resolution would secure more uniform implementation, to ensure that whatever agreements are made, they are properly enforced. This is a highly vexed question which has yet to be resolved.

Sixth, instead of looking for all-embracing free trade agreements such as TTIP, which actually don't really work, there is the prospect of "unbundling", seeking sector-specific solutions. This is an alternative to the grandiose free trade agreements that promise much and deliver little.

Seventh, there are openings for more constructive ways of dealing with freedom of movement â especially on a global level - and, finally, we address the issue of free movement of capital and payments.

Each of these eight points will, in due course, be the subject of a separate post, the overall point being that these alone are enough to shape the future and give us plenty of meat to work on. I would not see this programme being completed in 30 years, by which time other priorities will have emerged. That is not as bad as it sounds, though, because progress is being made all the time.

The dominant ethos of flexible response, coupled with continuous development, though, will never change. And that is why "Brexit" is actually a

chimera, and why anything that is offered as a fixed point or single event is a complete waste of space. Essentially, despite Myddelton's "

Ratner moment", it is FLexCit or nothing. As an event, "Brexit" simply cannot work.

FORUM THREAD